You’ve spent your career saving and investing with care. But in retirement, taxes don’t necessarily disappear — they often just become less obvious. One potential pitfall for higher-income retirees is IRMAA: an income-based surcharge on Medicare premiums that could quietly reduce your net retirement income if not proactively addressed.

IRMAA stands for Income-Related Monthly Adjustment Amount. It applies to Medicare Part B and Part D premiums and is based on your Modified Adjusted Gross Income (MAGI). If your income exceeds certain thresholds, you may be subject to higher monthly premiums.

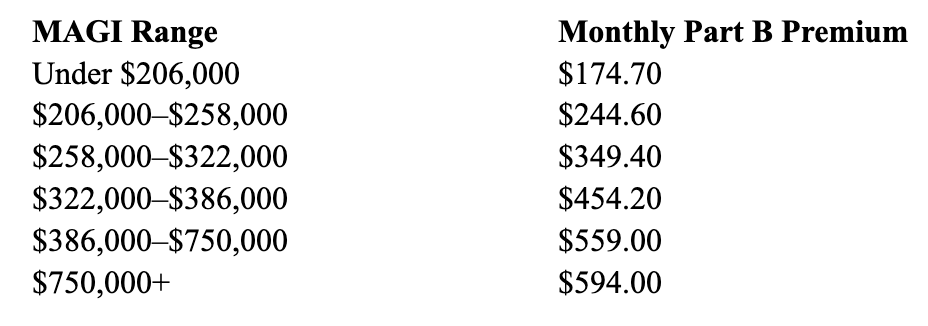

For 2025, the brackets look like this (Married Filing Jointly):

Note: IRMAA is determined using your income from two years prior. So your 2025 Medicare premiums are based on your 2023 tax return.

1. Time Roth Conversions Thoughtfully

Making Roth conversions in the early years of retirement — particularly before enrolling in Medicare — may help reduce required minimum distributions (RMDs) later, potentially minimizing future IRMAA exposure.

2. Manage Income Fluctuations

Avoiding large income spikes — whether from capital gains, pensions, or Social Security — can help smooth out MAGI. Thoughtful timing and coordination may allow you to stay within a lower IRMAA bracket.

3. Use Qualified Charitable Distributions (QCDs)

If you’re 70½ or older, QCDs can provide a way to meet RMD obligations while excluding the distributed amount from your taxable income, possibly reducing your MAGI.

Higher Medicare premiums due to IRMAA are not always unavoidable, but they can often be mitigated with proactive planning. For households with substantial retirement savings, strategies like these may lead to meaningful savings over time.

Want to explore how IRMAA might affect your retirement plan — and what strategies could work for you?

Schedule a Complimentary 15-Minute Retirement Tax Strategy Call

Securities offered through LPL Financial, member FINRA/SIPC. Investment Advice offered through Convergence Financial, a registered investment advisor. Convergence Financial and Telos Strategic Wealth are separate entities from LPL Financial.

Sources and References

Enter your email to instantly access "5 Questions to Ask When Meeting With a Financial Advisor" your free guide and ensure you're asking the right questions before working with a financial advisor.

.png)

.png)

.png)